Owner Financing vs. Traditional Mortgages: Which is Right for You?

Lisbet Newton • March 4, 2026

Deciding how to fund your home is one of the most significant financial decisions you’ll ever make.

For decades, the "Gold Standard" has been the 30-year fixed-rate bank mortgage. However, as lending requirements have tightened and the "gig economy" has grown, the traditional path has become a closed door for millions of qualified buyers.

If you’re weighing your options, it’s essential to understand how Owner Financing stacks up against a Traditional Mortgage. This article was created to share with you the differences between the two.

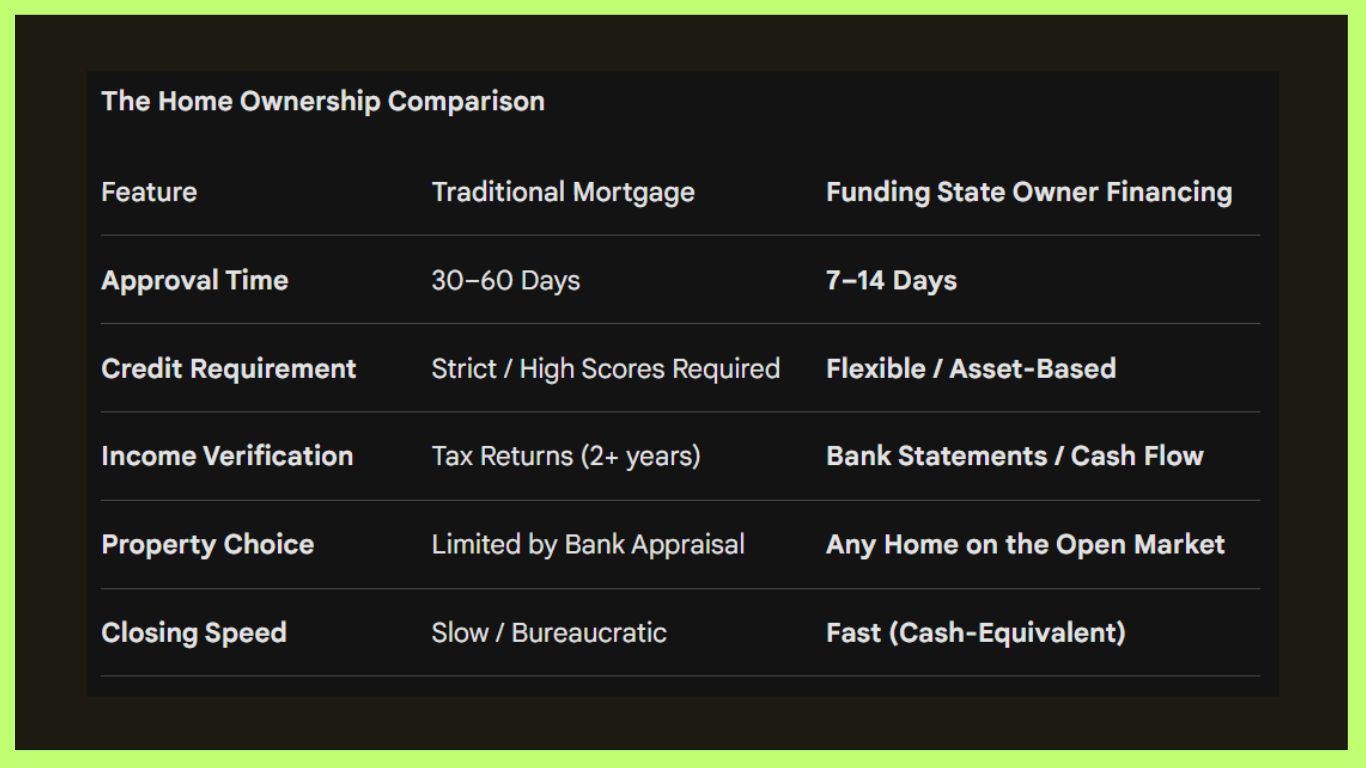

The Traditional Mortgage:

The "By-the-Book" Approach Traditional loans (FHA, VA, or Conventional) are managed by large institutional banks. They offer the lowest interest rates, but they come with a "one-size-fits-all" mentality.

- The Hurdles: Banks require a near-perfect "paper trail." If you have a gap in employment, a recent credit event, or you’re a business owner with heavy tax deductions, you may be disqualified regardless of how much cash you have in the bank.

- The Timeline: A standard bank closing can take 45 to 60 days. In a competitive market, sellers often pass over bank-financed offers in favor of cash.

- The Red Tape: You are at the mercy of an anonymous underwriter who may demand additional documentation at the eleventh hour.

Owner Financing: The Flexible Alternative

Owner financing (also known as a Seller Carry-back or Private Lending) is a private agreement between you and the funding entity. It functions much like a bridge, getting you into the home now while you build equity and credit.

- Approval Based on Reality: We look at your down payment and your current ability to pay, rather than a credit score from five years ago. This makes it the premier choice for self-employed individuals.

- Speed is a Competitive Edge: Because we aren't waiting on a bank's bureaucracy, we can close in as little as 10–14 days. This makes your offer as strong as a cash buyer’s.

- No "Invisible" Fees: Traditional loans often come with "origination points," "funding fees," and "private mortgage insurance (PMI)" that can add hundreds to your monthly payment. With owner financing, the terms are transparent and straight forward.

The "Opportunity Cost" of Waiting

Many people think, "I’ll just wait two years to fix my credit so I can get a bank loan." However, in a rising market, that same house might cost $50,000 more in two years. By choosing owner financing today, you capture the appreciation of the home and stop paying rent, which is a 0% return on your money.

Is Owner Financing for You? This path is ideal if you have a solid down payment and a stable income but don't "fit the box" of a traditional bank. It allows you to stop being a spectator in the real estate market and start being an owner.

Ready to compare your specific numbers? Contact me today to see how we can make the math work for you.

Contact Us

The traditional mortgage process often feels like an uphill battle against red tape, rigid credit scores, and endless paperwork. For many hardworking individuals, entrepreneurs, those relocating, or those with non-traditional credit, the dream of homeownership stays stuck behind a bank’s "No." At Funding State , we believe your ability to own a home should be based on your future potential, not just your past paperwork. Our streamlined owner-financing model is designed to put the keys in your hands faster through a clear, four-step journey. 1. Establish Your Buying Power (Pre-Qualification) Before you hit the pavement, you need to know exactly where you stand. Our pre-qualification process is fast and transparent. Unlike a traditional bank that might spend weeks "underwriting" your life story, we focus on your current financial stability and down payment capability. Within a short time, you’ll have a certified budget, allowing you to shop with the confidence of a cash buyer. 2. Shop the Open Market We don't limit you to a small "inventory" of distressed houses. Once you are pre-qualified, the entire market is open to you. Whether it’s a quiet suburban cul-de-sac in Cinco Ranch or a 1960's mid modern home in Bellaire, you find the home that fits your family’s needs. You bring us the property, and we bring the capital. 3. The Guaranteed Cash Closing In today’s competitive real estate market, cash is king. When you find "the one," we step in to purchase the property outright. By removing the "mortgage contingency" from the deal, we make your offer significantly more attractive to sellers. We handle the professional inspections, title work, and closing costs, ensuring the transaction is legally sound and secure. 4. Move In & Start Building Equity Once the purchase is complete, we provide the owner financing directly to you. You move in immediately as the resident owner. Instead of throwing money away on monthly rent, every payment you make contributes to your future. Our flexible terms are designed to act as a bridge, giving you the time and space to build equity and eventually transition into traditional financing on your own timeline. Why Choose This Path? Speed : Close in days or weeks, not months. Freedom : Choose any home on the market that meets our safety standards. Inclusion : We say "Yes" when banks say "No" due to self-employment, credit issues, etc. Stop Waiting, Start Owning. The path to your new front door doesn't have to be a maze. Contact us today for more information and see how close you really are to homeownership.

In the world of real estate, "different" can sometimes feel "risky." If you’ve only ever heard of traditional bank mortgages, the concept of owner financing might raise a few questions. Is it legal? Is my investment protected? How does the paperwork work? At Funding State, transparency is our north star. We want you to go into your closing with total peace of mind. Here are the three pillars of security that define our owner-financing process. 1. It is a Fully Legal, Recorded Real Estate Transaction Owner financing is not a "handshake deal" or a casual rental agreement. It is a formal real estate closing conducted through a licensed title company or real estate attorney. The Deed: Just like a bank sale, the transfer of the property is recorded with the county. The Note & Deed of Trust: You will sign a Promissory Note (your promise to pay) and a Deed of Trust (which secures the property). These are the same legal instruments used by major banks like Chase or Wells Fargo. Your Rights: You have the legal rights of a homeowner, including the right to homestead the property, make improvements, and benefit from tax deductions on mortgage interest. 2. Professional Title Insurance is Non-Negotiable We never bypass the safety checks. Before any money changes hands, a professional title company performs a comprehensive search to ensure the property is free of "clouds" (like hidden liens, unpaid taxes, or ownership disputes).We require Title Insurance on every transaction. This protects your equity and ensures that your claim to the home is undisputed. You can sleep soundly knowing that your investment is legally fortified against any past claims on the property. 3. You Have an "Exit Strategy" Built-In Most people view owner financing as a bridge, not a forever destination. Our contracts are designed with your future in mind. No Pre-Payment Penalties: In our agreements, our goal is to refinance you within 12 months into a traditional bank loan because your credit has improved, you can do so without penalty. Refinance Ready: We provide you with a clear payment history. When you are ready to transition to a traditional mortgage, you can show the bank a consistent record of on-time payments, making your future "conventional" approval much easier.

Traditional lenders rely on a specific set of rules that haven’t caught up with the modern economy. At Funding State, we understand that your tax return doesn't tell your whole story. Here is why owner financing is the preferred "Power Move" for the self-employed. The Problem: The "Tax Return Trap" Most traditional mortgage underwriters look at your Adjusted Gross Income (AGI)—the number after you’ve taken all your legal business deductions. While those deductions are great for your tax bill, they shrink your "official" income in the eyes of a bank. To a traditional lender, you look like a risk. To us, those deductions look like a smart business strategy. We don't penalize you for being a savvy business owner. How We Qualify You Differently Instead of obsessing over two years of perfect tax returns, we look at the real-world indicators of your financial health: Bank Statement Consistency: We look at your actual deposits and cash flow over the last 12–24 months. Skin in the Game: A strong down payment shows us you are committed and capable, regardless of what a credit bureau says. Asset Value: Since we are purchasing the home, we focus on the quality of the real estate asset you’ve chosen. The Benefits of Staying "Bank-Free" Preserve Your Time: As a business owner, your time is your most valuable asset. Chasing down obscure documents for a bank auditor for three months is a massive distraction from growing your company. Our process is built for speed. No "Debt-to-Income" Deadlocks: Banks often calculate your DTI (Debt-to-Income ratio) using personal and business debts. We offer more flexible ratios that account for the reality of running a company. Capture Appreciation Early: Waiting two years to "fix" your tax returns just to qualify for a bank loan means missing out on two years of market growth. Owner financing lets you lock in today’s home price while your business continues to scale. A Bridge to Your Future Many of our entrepreneurial clients use owner financing as a strategic bridge. They move into the home now, enjoy the tax benefits of homeownership (like mortgage interest deductions), and eventually "buy us out" or refinance into a traditional loan once their business cycles allow for a cleaner paper trail. Your business didn't settle for "average," and your home shouldn't either. Don't let a bank's rigid boxes stop your progress. Schedule a Strategy Call to see how we can turn your business success into a new front door.